📊 Full opportunity report: The license. Why the AI content market pays the brand-name corpus and strands the long tail. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

Large publishers secure licensing deals with AI companies, capturing value from their brand-name archives. Small publishers are largely excluded, reinforcing existing inequalities in the AI content market. The key question is whether collective licensing can address this imbalance.

Large publishers have secured substantial licensing agreements with AI companies, capturing the value of their brand-name archives, while small publishers are largely excluded from these deals.

Recent disclosures reveal that major publishers such as News Corp, the Associated Press, and major newspapers have signed multi-million dollar licensing deals with AI firms like OpenAI and Meta. These agreements, often exceeding $50 million annually, give AI companies access to high-trust, brand-name corpora, which are essential for training and grounding large language models.

In contrast, smaller publishers—niche sites and independent outlets—are rarely part of these licensing arrangements. Their content, which is abundant and less distinctive, is often scraped without compensation, and they lack the leverage to negotiate licensing terms. This disparity creates a structural asymmetry: large publishers benefit from scarcity and branding, while small publishers are left vulnerable to being commodified for free training data.

The pattern reflects a winner-take-all dynamic, where the value of content is concentrated among a few large entities, reinforcing existing inequalities in the digital news ecosystem.

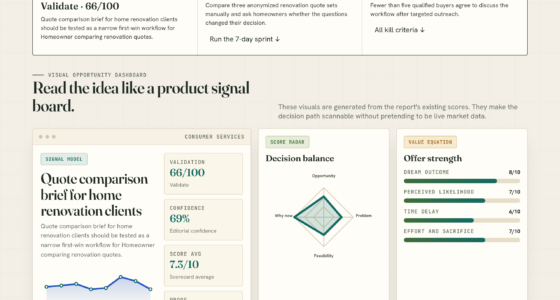

The license.

Why the AI content market

pays the brand-name corpus

and strands the long tail.

licensing deal below it

the large-publisher reality

largest licensing deal · a rounding error

tail’s most direct shot, via aggregation

↓

leverage

↓

a fee

The license that saved the Wall Street Journal does not reach the niche site, and the only thing that could is a market the small publisher cannot build alone. The escape route is real. For most of the publishers who needed it, it leads to a door they cannot open.Thorsten Meyer · The License · Post-Wire 04

Implications of Licensing Concentration for Small Publishers

This licensing asymmetry confirms that the current market favors large, brand-name publishers, perpetuating the decline of small publishers and independent outlets. It underscores a structural imbalance: the market rewards scarcity and leverage, which small publishers lack, effectively marginalizing their content.

Without intervention, this trend risks further consolidation of media power and a less diverse information landscape. The only potential remedy is the development of collective or statutory licensing regimes, which could ensure fair compensation for all publishers regardless of size, but such mechanisms remain unproven at scale and face opposition from platforms and AI firms.

The Business of Media Distribution (American Film Market Presents)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Background on AI Licensing and Publisher Disparities

The collapse of referral traffic from AI search and chat interfaces has pushed publishers to seek direct licensing agreements as an alternative revenue source. Large publishers, with high-value archives and brand recognition, have successfully negotiated multi-million dollar deals with AI companies, establishing a lucrative licensing market.

Small publishers, however, have been largely excluded from these arrangements, as their content is plentiful and less distinctive. This has resulted in a structural asymmetry: large publishers profit from their scarcity and branding, while small publishers see their content scraped without compensation. The current licensing landscape thus reproduces the inequalities it was supposed to address.

Efforts to establish collective licensing systems—similar to music royalties—are underway, but these are still in development and face legal and political hurdles. The broader debate centers on whether such regimes can be scaled to effectively support small publishers and restore a balanced market.

“The licensing market reproduces the same asymmetry it was meant to solve—value flows to the brand-name corpus, while the long tail provides data for free.”

— Thorsten Meyer

AI for Small Business: From Marketing and Sales to HR and Operations, How to Employ the Power of Artificial Intelligence for Small Business Success (AI Advantage)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Prospects for Collective Licensing Implementation

It remains uncertain whether collective or statutory licensing regimes will be successfully implemented at scale before many small publishers are pushed out of the market entirely. Legal, political, and platform opposition pose significant hurdles, and the timing of any such system remains uncertain.

How to Start, Run, and Grow a Home Inspection Business: The A-Z Guidebook for New Entrepreneurs -Includes 50 States plus Washington DC Licensing Requirements

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps for Addressing Licensing Inequities

Efforts are ongoing to develop collective licensing frameworks, including proposals from the UK coalition, EU initiatives, and WIPO. The success of these initiatives depends on legal rulings, platform cooperation, and political support. Monitoring these developments will determine whether a viable, equitable licensing system can be established before small publishers are further marginalized.

Best AI Tools for Content Creators (2026 Edition): Grow Faster on on YouTube, Instagram & Social Media Using ChatGPT & Powerful AI Tools

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why do large publishers secure bigger licensing deals than small publishers?

Large publishers have high-value, brand-name archives that AI companies want access to for training and grounding models. Their content carries leverage due to scarcity and trustworthiness, enabling them to negotiate larger deals.

Are small publishers completely excluded from licensing agreements?

Yes, most small publishers are not part of these licensing deals because their content is abundant and less distinctive, making it less attractive for licensing and easier for AI companies to scrape without compensation.

Could collective licensing solve the inequality problem?

Collective or statutory licensing could ensure fair compensation for all publishers regardless of size, but such systems are still in development and face significant legal and political obstacles.

What are the risks if small publishers are left out of licensing?

Excluding small publishers risks further concentration of media power, loss of diversity in information sources, and a decline in independent journalism, as their content becomes commodified without compensation.

What is the main challenge in establishing a fair licensing system?

The main challenge is creating a scalable, legally sound framework that balances the interests of large publishers, small publishers, AI companies, and platforms, and gaining broad political and platform support.

Source: ThorstenMeyerAI.com